China Heat Exchanger Market Size, Share, Top Companies, Forecast 2025-2033

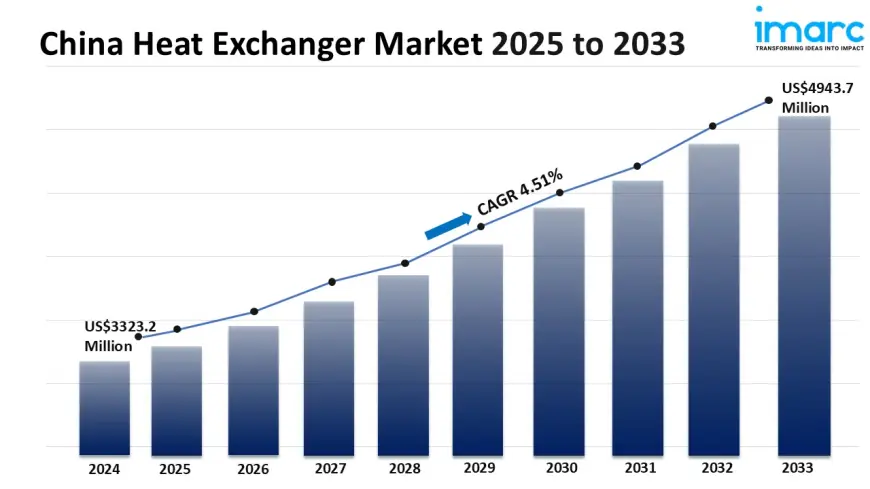

The China heat exchanger market size reached USD 3,323.2 Million in 2024. Looking forward, IMARC Group expects the market to reach USD 4,943.7 Million by 2033, exhibiting a growth rate (CAGR) of 4.51% during 2025-2033.

China Heat Exchanger Market Overview

Base Year: 2024

Historical Years: 2019-2024

Forecast Years: 2025-2033

Market Size in 2024: USD 3,323.2 Million

Market Forecast in 2033:USD 4,943.7 Million

Market Growth Rate (2025-33): 4.51%

The China heat exchanger market size reached USD 3,323.2 Million in 2024. Looking forward, IMARC Group expects the market to reach USD 4,943.7 Million by 2033, exhibiting a growth rate (CAGR) of 4.51% during 2025-2033. Rapid industrialization and urbanization, expanding heating, ventilation, and air conditioning (HVAC) sector growth, energy efficiency mandates, stringent environmental regulations, booming chemical industry, automotive industry expansion, investments in renewable energy, and the growing food and beverage sector are some of the factors propelling the market growth.

For an in-depth analysis, you can refer sample copy of the report: https://www.imarcgroup.com/china-heat-exchanger-market/requestsample

China Heat Exchanger Market Trends and Drivers:

The Chinese heat exchanger market is undergoing a profound transformation fundamentally driven by the nation's aggressive "Dual Carbon" goals (carbon peak by 2030, carbon neutrality by 2060) and the overarching 14th Five-Year Plan mandates for industrial energy efficiency. This policy environment is catalyzing unprecedented demand for highly efficient heat transfer solutions across critical sectors. Power generation, particularly the rapid expansion of renewables like concentrated solar power (CSP) and biomass co-firing plants, alongside the strategic development of next-generation nuclear reactors (e.g., High-Temperature Gas-Cooled Reactors requiring specialized heat exchangers), is a primary growth engine. Simultaneously, stringent new energy efficiency standards (GB standards) are forcing retrofits and replacements in vast industrial facilities like petrochemical complexes, chemical plants, and iron & steel mills, where heat exchangers are pivotal for waste heat recovery and process optimization. Government subsidies and preferential loans for energy-saving retrofits further accelerate this replacement cycle. Future demand is intrinsically linked to the depth and enforcement of these decarbonization policies, pushing innovation towards compact designs, advanced materials resisting harsh conditions, and systems maximizing heat recovery potential, creating a sustained, policy-anchored growth vector for sophisticated heat exchanger technologies.

The competitive landscape and future demand within China's heat exchanger market are increasingly defined by rapid technological innovation, moving beyond traditional manufacturing towards smart, integrated solutions. Advanced materials like super duplex stainless steels, titanium alloys, nickel-based alloys, and specialized coatings are gaining traction, driven by demands for corrosion resistance in chemical processing, desalination, and harsh flue gas environments, enabling longer lifespans and lower lifecycle costs. Concurrently, additive manufacturing (3D printing) is transitioning from prototyping to production, allowing for complex geometries (e.g., optimized internal fin structures) impossible with conventional methods, significantly enhancing thermal efficiency and compactness for applications like aerospace and high-performance cooling. Crucially, digitalization is revolutionizing the sector: integration of Industrial Internet of Things (IIoT) sensors enables real-time performance monitoring, predictive maintenance algorithms drastically reducing unplanned downtime, and digital twins optimize operational parameters. This convergence of materials science, advanced manufacturing, and digital intelligence creates high-value products meeting evolving customer needs for reliability, efficiency, and data-driven operational insights, shaping future market leadership.

While traditional heavy industries remain significant, future demand growth for heat exchangers in China is increasingly propelled by diversification into vibrant, high-potential sectors. The electrification mega-trend, particularly the explosive growth of New Energy Vehicles (NEVs) and associated battery manufacturing, demands highly efficient thermal management systems (battery cooling/heating, power electronics cooling) utilizing compact plate, microchannel, and cold plate heat exchangers. Data center proliferation, driven by cloud computing and AI, necessitates massive, reliable cooling capacity, favoring large-scale plate-and-frame and brazed plate heat exchangers for chilled water systems. Furthermore, stringent environmental regulations on wastewater treatment and ambitious desalination projects to address water scarcity drive demand for corrosion-resistant shell & tube and plate heat exchangers. The burgeoning hydrogen economy, encompassing both production (electrolyzer cooling) and fuel cell applications, represents another frontier requiring specialized thermal solutions. This diversification mitigates reliance on cyclical heavy industries, creating a more resilient market with sustained growth drivers rooted in China's strategic technological and environmental priorities, demanding versatility and application-specific innovation from suppliers.

China Heat Exchanger Market Industry Segmentation:

Type Insights:

- Shell and Tube

- Plate and Frame

- Air Cooled

- Others

Material Insights:

- Carbon Steel

- Stainless Steel

- Nickel

- Others

End Use Industry Insights:

- Chemical

- Petrochemical and Oil & Gas

- HVAC and Refrigeration

- Food & Beverage

- Power Generation

- Paper & Pulp

- Others

Region Insights:

- North China

- East China

- South Central China

- Southwest China

- Northwest China

- Northeast China

Competitive Landscape:

The competitive landscape of the industry has also been examined along with the profiles of the key players.

Ask Our Expert & Browse Full Report with TOC & List of Figure: https://www.imarcgroup.com/request?type=report&id=23405&flag=C

Key highlights of the Report:

- Market Performance (2019-2024)

- Market Outlook (2025-2033)

- COVID-19 Impact on the Market

- Porter’s Five Forces Analysis

- Strategic Recommendations

- Historical, Current and Future Market Trends

- Market Drivers and Success Factors

- SWOT Analysis

- Structure of the Market

- Value Chain Analysis

- Comprehensive Mapping of the Competitive Landscape

Note: If you need specific information that is not currently within the scope of the report, we can provide it to you as a part of the customization.

About Us:

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provide a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel No:(D) +91 120 433 0800

United States: +1-201971-6302

What's Your Reaction?

Like

0

Like

0

Dislike

0

Dislike

0

Love

0

Love

0

Funny

0

Funny

0

Angry

0

Angry

0

Sad

0

Sad

0

Wow

0

Wow

0