Premium Chocolate Market — Market Brief (2024–2032)

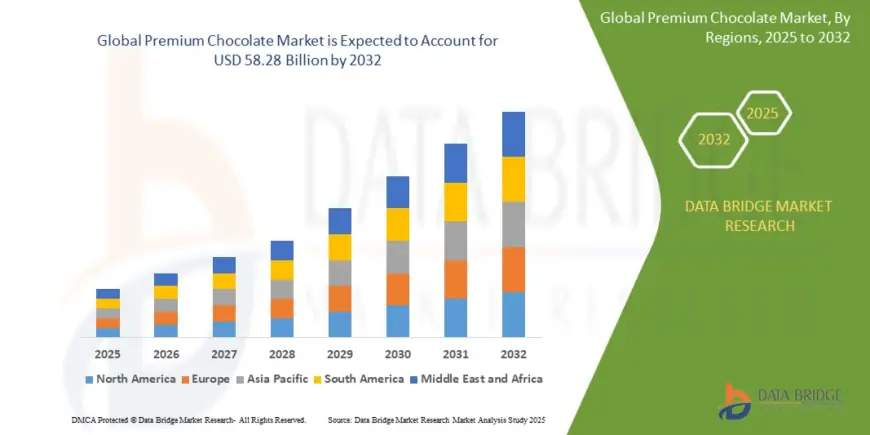

The global premium chocolate market was valued at USD 41.61 billion in 2024 and is expected to reach USD 58.28 billion by 2032

Executive summary

Premium chocolate is the higher-end segment of the broader chocolate market, defined by superior cocoa sourcing (single-origin or traceable blends), higher cocoa percentages, artisanal production, premium packaging, ethical/sustainable credentials, and culinary innovation. The segment commands higher price points and enjoys resilient demand from affluent consumers, gifting seasons, and foodservice channels.

Source - https://www.databridgemarketresearch.com/reports/global-premium-chocolate-market

Working estimates:

-

Global premium chocolate market (2024): roughly USD 25–30 billion.

-

Expected CAGR (2024–2032): 5–8%.

-

Indicative market size (2032): USD 40–55 billion, depending on premiumization and penetration in emerging markets.

Key demand drivers

-

Premiumization and willingness to pay — consumers trade up for perceived quality, origin story, and sensory experience (flavor complexity, bean-to-bar craftsmanship).

-

Health & higher-cocoa formulations — demand for dark chocolate (higher cocoa solids) linked to antioxidant positioning and lower sugar profiles.

-

Ethical and sustainability credentials — traceability, fair pay, agroforestry, organic and Rainforest/ethics claims drive purchasing among conscious consumers.

-

Gift and seasonal demand — premium chocolates are a staple for holidays, corporate gifting and luxury hospitality.

-

Experiential & culinary trends — chef collaborations, limited editions, filled ganaches, and crossover formats (chocolate + tea/spirits) increase appeal.

-

E-commerce & D2C brands — direct channels enable premium niche brands to reach global buyers with storytelling and subscriptions.

Market segmentation

By product type

-

Single-origin / bean-to-bar bars

-

Pralines, bonbons, filled/ganache confections

-

Single-serve gourmet snacks & small-batch truffles

-

Drinking chocolate and ready-to-drink premium chocolate beverages

-

Coated premium confections (nuts, fruit)

By positioning / credentials

-

Craft / artisanal brands

-

Luxury / heritage brands (legacy chocolatiers)

-

Organic / fair trade / direct-trade certified

-

High-cocoa / functional (added probiotics, adaptogens)

By distribution channel

-

Specialty retail & chocolatier stores

-

Supermarkets / premium grocery chains

-

Duty-free & travel retail (high margin)

-

E-commerce / D2C subscriptions

-

Foodservice (luxury hotels, fine dining, patisseries)

By geography

-

Mature markets: Western Europe, North America, Japan

-

High-growth markets: China, Southeast Asia, Middle East, affluent segments in Latin America

Regional dynamics

-

Europe: Historic demand for premium chocolate (Belgium, Switzerland, France) with high per-capita spend and strong gifting culture. Premium dark chocolate and single-origin bars do well.

-

North America: Large premium confectionery market; craft and bean-to-bar brands grow alongside established luxury players; D2C subscriptions and experiential retail are powerful growth channels.

-

Asia (China, Japan, Korea): Fastest premiumization — luxury gifting, rising middle/upper classes, and in-store premium experiences (flagships). Local artisanal brands emerging.

-

Middle East: High demand for luxury gifting and hospitality; premium packaging and limited editions perform strongly.

-

Latin America & Africa: Increasing domestic premium producers (near cocoa origin) but most premium brands currently imported.

Consumer trends and preferences

-

Shift toward higher cocoa percentages and lower sugar formulations.

-

Desire for transparent origin stories and farmers’ welfare information.

-

Interest in novel flavor pairings (savory notes, spices, floral/citrus) and texture innovations.

-

Growing preference for premium sustainable packaging (recyclable, reusable boxes).

-

Younger consumers attracted by limited drops, collaborations, and social media storytelling.

Competitive landscape & value chain

-

Large luxury confectioners (heritage brands) dominate gift and travel retail channels.

-

Specialist bean-to-bar and craft chocolatiers compete on provenance, small-batch production, and direct-trade narratives.

-

Private-label premium ranges from supermarkets target value-conscious premium buyers.

-

Ingredient and co-packer ecosystem supplies ganache, inclusions, and premium fillings at scale.

-

Distribution dynamics: Established brands rely on premium retail and travel retail; new entrants use D2C and boutique wholesale to fine dining and luxury hotels.

Pricing and margins

-

Premium chocolate prices vary widely by format, origin, and channel: small-batch single-origin bars, artisan bonbons, and gift boxes carry bandwidths from mid-premium to ultra-luxury price points.

-

Margins are highest for direct-to-consumer and bespoke B2B (hotel / gifting) contracts due to brand premium and lower middle-man costs. Retail private label narrows margins but offers scale.

Innovation & product development

-

Functional premium chocolate: added adaptogens, vitamins, or pre/probiotics positioned for wellness.

-

Sustainable innovation: regenerative cocoa sourcing and low-impact supply chains.

-

Packaging innovation: premium unboxing experiences, reusable tins, and minimal waste formats.

-

Format diversification: chocolate-infused beverages, culinary chocolate for chefs, and confectionery hybrids.

-

Traceability tech: QR codes and blockchain for provenance verification and storytelling.

Risks & challenges

-

Cocoa price volatility and supply risk — weather, pests and political instability in origin countries affect cost and availability.

-

Authenticity and adulteration — premium claims must be backed by traceability to avoid reputational damage.

-

Sustainability compliance costs — higher sourcing and certification costs can compress margins if not passed to consumers.

-

Health & regulatory scrutiny — sugar reduction trends and health labeling may challenge some premium indulgent segments.

-

Competition & market saturation — proliferation of small artisan brands increases noise; brand differentiation is critical.

-

Packaging sustainability — premium packaging must balance luxury with environmental expectations.

Channel & go-to-market recommendations

For premium brand owners

-

Invest in traceable origin stories and clinical/technical messaging for functional claims.

-

Use D2C subscriptions and limited drops to build direct relationships and recurring revenue.

-

Secure partnerships with premium hotels, airlines and selected retailers for visibility and margin.

-

Prioritize sustainable packaging and certifications to support premium positioning.

For retailers & distributors

-

Curate premium lines with clear provenance and tasting notes; train staff for sensory selling.

-

Use seasonal and experiential merchandising (tasting stations, pairing events) to increase average basket value.

-

Leverage travel retail and corporate gifting channels for high-margin volume.

For investors

-

Favor vertically integrated models (control over sourcing and extraction) or brands with demonstrable D2C traction and repeat purchase metrics.

-

Look for companies with scalable manufacturing or co-packing partnerships and strong IP/brand equity.

Forecast snapshot (decision-ready)

| Metric | 2024 (est.) | 2032 (proj.) |

|---|---|---|

| Market size (global premium chocolate) | USD 25–30 billion | USD 40–55 billion |

| CAGR (2024–2032) | 5–8% | — |

| Fastest-growing regions | Asia (China, SEA), Middle East | — |

| Highest-margin channels | D2C, travel retail, B2B gifting | — |

Conclusion

The premium chocolate market combines emotional purchase drivers (gifting, indulgence) with rational drivers (quality, provenance, sustainability). Long-term growth is robust where brands can combine authentic origin stories, sensory excellence, and credible sustainability credentials while scaling through D2C and premium retail channels. Managing cocoa supply risk, proving authenticity, and aligning premium packaging with sustainability expectations will separate winners from followers.

What's Your Reaction?

Like

0

Like

0

Dislike

0

Dislike

0

Love

0

Love

0

Funny

0

Funny

0

Angry

0

Angry

0

Sad

0

Sad

0

Wow

0

Wow

0