Advancements in Carbon Capture Technology to Revolutionize Environmental Efforts

Carbon Capture and Storage Market By Technology (Pre-combustion, Post-combustion, Oxy-combustion, and Industrial Process), By End-Use Industry (Power Generation, Oil & Gas, and Other End-Use Industries), By Region and Companies – Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, and Forecast 2023 – 2032

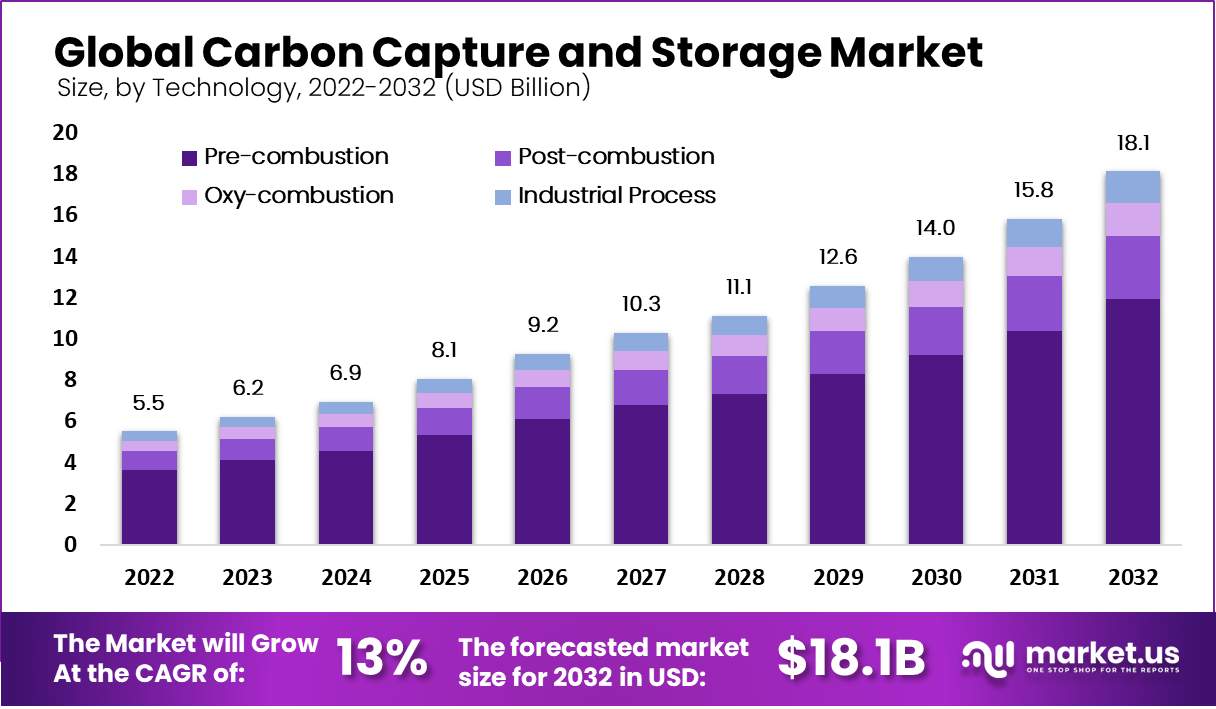

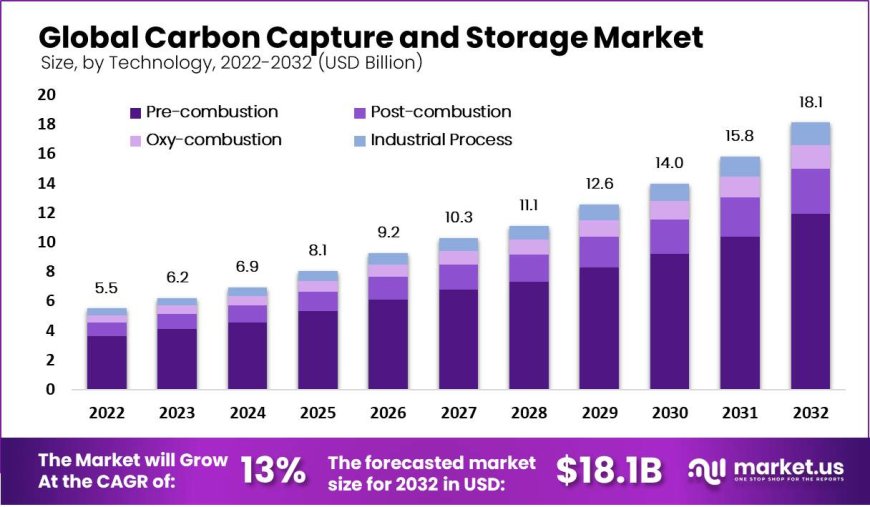

Carbon Capture and Storage Market size was valued at USD 5.5 Billion. This market is estimated to reach USD 18.1 Billion in 2032 the highest CAGR of 13% between 2023 and 2032.

The Carbon Capture and Storage (CCS) market involves technologies and processes designed to capture carbon dioxide (CO₂) emissions from industries like steel and cement production or power plants that burn fossil fuels. Once captured, this CO₂ is transported—usually via pipelines or ships—to storage sites.

Get a Sample Copy with Graphs & List of Figures @ https://market.us/report/carbon-capture-and-storage-market/request-sample/

These sites are typically deep underground geological formations where the CO₂ is securely stored, preventing it from entering the atmosphere. The main goal of CCS is to reduce greenhouse gas emissions, mitigating the effects of global warming and climate change by keeping CO₂ out of the air.

As industrialization and global population growth continue to rise, so does the demand for goods and services that often rely on fossil fuels, which in turn increases CO₂ emissions. This growing environmental concern drives the need for effective carbon capture and storage solutions.

By capturing and storing CO₂, CCS helps to lower the carbon footprint of industrial activities and contributes to global efforts to combat climate change. As a result, the CCS market is expanding as more companies invest in and adopt these technologies to meet environmental regulations and sustainability goals.

Key Market Segments :

By Technology :

-

Pre-combustion

-

Post-combustion

-

Oxy-combustion

-

Industrial Process

By End-Use Industry :

-

Power Generation

-

Oil & Gas

-

Metal Production

-

Cement

-

Other End-Use Industries

Pre-combustion technology leads the global carbon capture and storage market, commanding a significant revenue share of 65.8%. This dominance is driven by its efficient CO₂ capture capabilities using water gas shift reactions and acid gas removal, coupled with its lower energy penalties. In the end-use industry segment, power generation holds the largest market share at 64.6%.

This is largely due to coal-fired power plants being major CO₂ emitters, necessitating CCS to meet stringent emissions regulations and reduce carbon footprints.

Top Key Players :

-

Siemens AG

-

Aker Solutions

-

Dakota Gasification Company

-

Fluor Corp.

-

Linde plc

-

Mitsubishi Heavy Industries Ltd.

-

Equinor ASA

-

Royal Dutch Shell PLC

-

Sulzer Ltd.

-

Exxon Mobil Corporation

-

Other Key Players

Driving Factor:

Rising environmental concerns and advancements in gas injection enhanced oil recovery (EOR) techniques are fueling the growth of the carbon capture and storage (CCS) market. As industrialization and urbanization increase emissions, CCS offers a solution to mitigate environmental harm by capturing and storing CO₂. Additionally, CCS is used in EOR to extract crude oil, boosting its market appeal as oil reservoirs deplete.

Restraining Factor:

Safety concerns and high costs are major constraints for the CCS market. Risks associated with CO₂ storage, such as leakage and environmental hazards, necessitate rigorous monitoring and safety measures. Moreover, the high investment required for CCS technology makes it challenging for smaller companies to adopt.

Opportunity:

Technological advancements, particularly in pre-combustion technology, present significant opportunities for market growth. Pre-combustion offers efficient CO₂ capture with lower energy penalties, driving its dominance in the CCS sector and expanding its application across industries.

Challenge:

The high cost of implementing CCS technology and maintaining safety standards is a key challenge. Ensuring effective monitoring and preventing potential hazards in underground storage sites can be complex and costly, impacting the market’s broader adoption and growth.

What's Your Reaction?

Like

0

Like

0

Dislike

0

Dislike

0

Love

0

Love

0

Funny

0

Funny

0

Angry

0

Angry

0

Sad

0

Sad

0

Wow

0

Wow

0