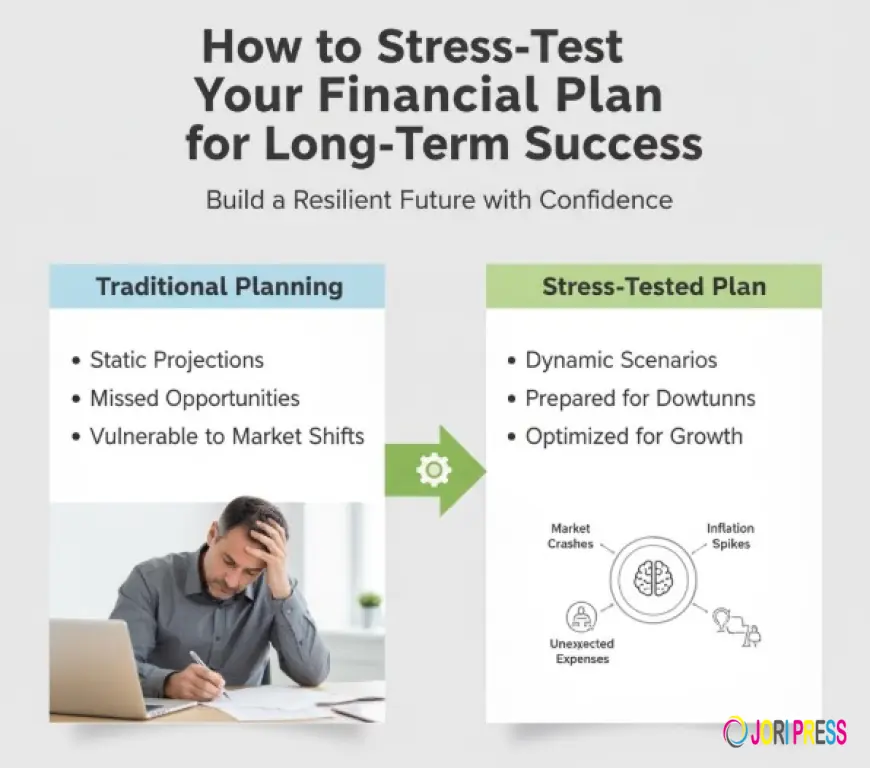

How to Stress-Test Your Financial Plan for Long-Term Success

When it comes to managing money, most people have a financial plan — but very few test it against reality. Think about it like this: would you buy a car without checking if it could handle rough roads? Probably not. The same logic applies to your finances. Your plan might look perfect on paper, but what happens when life throws you a curveball like a job loss, market crash, or medical emergency? That’s where stress-testing your financial plan comes into play.

Let’s dive into how you can put your plan through its paces and make sure it’s built to last — no matter what the economy (or life) throws at you.

What Is a Financial Stress Test?

A financial stress test is essentially a “what if” exercise. It’s a way to simulate worst-case scenarios to see how your finances would hold up.

For instance, imagine asking yourself:

-

What if the stock market drops by 30%?

-

What if I lose my job for six months?

-

What if inflation spikes and my expenses rise by 20%?

.The goal is to uncover weaknesses before they become real problems. Just like banks perform stress tests to ensure they can survive economic downturns, individuals can use this tool to protect their long-term wealth. To learn more about securing your financial future, visit RetireStrong Financial Advisors.

Why Stress-Testing Your Plan Matters

You might be thinking, “Isn’t that a bit too cautious?” Not at all. In fact, stress-testing isn’t about being pessimistic, it’s about being prepared.

Here’s why it’s so crucial:

-

It exposes blind spots. You might think your emergency fund or investments are solid until you run through a few tough scenarios.

-

It helps you sleep better. Knowing your plan can weather storms gives you real peace of mind.

-

It builds resilience. You’ll know exactly how to adjust your spending, savings, or investments if times get tough.

In short, stress-testing transforms your financial plan from “good” to “bulletproof.”

Key Areas to Stress-Test

Not every part of your finances needs the same level of scrutiny. Let’s break down the major areas you should test and how to do it effectively.

| Area | Why It Matters | How to Stress-Test It |

|---|---|---|

| Income Stability | A sudden job loss or income cut can derail your plan. | Simulate what happens if you lose your job or face a pay reduction. Can you cover your expenses for 3–6 months? |

| Expenses | Inflation and lifestyle creep can eat away at savings. | Add 10–20% to your current expenses and see if your budget still holds. |

| Investments | Markets fluctuate; volatility is inevitable. | Run scenarios for 20–30% market drops. How does that affect your retirement timeline? |

| Debt | High-interest debt can magnify financial stress. | Test your ability to keep up with payments during income disruptions. |

| Emergency Fund | Your financial safety net. | Check if your emergency fund can cover essential expenses for at least six months. |

How to Run a Financial Stress Test (Step-by-Step)

You don’t need fancy software or a finance degree to stress-test your plan. Just follow these simple steps.

Step 1: Gather Your Financial Information

Start by collecting all your numbers income, expenses, investments, savings, and debts. This gives you a clear snapshot of your financial situation.

Make sure to include:

-

Monthly income (salary, business earnings, etc.)

-

Fixed and variable expenses

-

Total savings and emergency funds

-

Investment portfolio breakdown

-

Outstanding debts and interest rates

This is your “baseline” before adding any stress scenarios.

Step 2: Identify Potential Risks

Every person’s risks are different. If you’re self-employed, your income might fluctuate. If you’re close to retirement, market downturns hit harder. Common risks include:

-

Job loss or pay cuts

-

Market crashes

-

Inflation spikes

-

Unexpected medical costs

-

Interest rate increases

-

Major home repairs or family emergencies

Pick the ones most relevant to your life.

Step 3: Run “What If” Scenarios

Now it’s time to test. Use a spreadsheet or financial planning tool and tweak the numbers to simulate those risks.

For example:

-

Reduce your income by 25% and see if you can still cover expenses.

-

Increase your expenses by 15% to simulate inflation.

-

Lower investment returns by 30% to mimic a market downturn.

You’ll quickly see how flexible (or fragile) your plan really is.

Step 4: Evaluate the Impact

After running the scenarios, look at how each one affects your financial stability. Are you still able to pay bills? Meet savings goals? Stay on track for retirement?

If your plan collapses under pressure, don’t panic that’s actually great news. It means you found the weak spots before reality did.

Step 5: Build Contingency Plans

Once you identify weaknesses, create strategies to fix them. This could include:

-

Increasing your emergency fund

-

Diversifying your investments

-

Cutting unnecessary expenses

-

Purchasing insurance (life, disability, or income protection)

-

Creating alternative income streams

The goal is to turn your “what ifs” into “I’m ready ifs.”

Common Stress-Test Scenarios

Here are a few of the most common (and realistic) financial stress scenarios you should run.

| Scenario | Potential Impact | How to Prepare |

|---|---|---|

| Job Loss | Loss of income and possible reliance on savings. | Build a 6–12-month emergency fund and explore side income options. |

| Market Crash | Investment value drops, delaying goals like retirement. | Diversify your portfolio and avoid panic selling. |

| Inflation Surge | Rising cost of living reduces spending power. | Invest in inflation-protected assets like real estate or TIPS. |

| Unexpected Health Issue | Medical bills and income disruption. | Maintain comprehensive health insurance and a health savings account (HSA). |

| Interest Rate Hike | Higher debt payments. | Refinance loans or pay off variable-rate debt early. |

Using Tools to Help You Stress-Test

While you can do this manually, several tools make the process easier:

-

Personal finance apps like YNAB or Mint for budgeting simulations.

-

Investment simulators like Portfolio Visualizer or Monte Carlo calculators to test market volatility.

-

Spreadsheets (Google Sheets or Excel) for custom “what if” models.

These tools allow you to visualize your outcomes and make data-driven adjustments.

The Emotional Side of Stress-Testing

Money isn’t just numbers, it’s deeply emotional. Running a stress test might make you uncomfortable, especially if it reveals vulnerabilities. But remember, discomfort now prevents disaster later.

It’s better to face potential financial pain in a spreadsheet than in real life. Plus, when you see your plan hold strong under pressure, your confidence skyrockets.

How Often Should You Stress-Test Your Financial Plan?

Financial stress-testing isn’t a one-time event. Life changes and so should your plan. You should review and update your test at least once a year, or whenever you experience major life changes such as:

-

A new job or business

-

Marriage or divorce

-

Buying a home

-

Having children

-

Significant investment or market shifts

Think of it like your annual health checkup — a routine that keeps you financially fit.

Building Resilience: The Real Goal

The point of stress-testing isn’t to avoid every possible problem that’s impossible. It’s about building flexibility and resilience so you can adapt when things go wrong.

Here’s how you can strengthen your financial resilience:

-

Diversify income sources. Multiple income streams can act as your safety net.

-

Invest wisely. Avoid putting all your money in one asset class.

-

Maintain liquidity. Keep a portion of your assets easily accessible.

-

Stay insured. Proper insurance protects against major financial shocks.

-

Keep learning. Financial literacy helps you make better decisions under pressure.

Long-Term Success Comes from Preparation

Let’s be honest financial success isn’t about getting lucky. It’s about staying ready.

You wouldn’t sail across the ocean without testing your boat against rough waves first. The same applies to your financial journey. Stress-testing ensures your plan can handle the storms ahead whether that’s a job loss, market crash, or unexpected expense.

And once you know your plan is solid, you can move forward with confidence, focus, and peace of mind.

Quick Recap: Your Financial Stress-Test Checklist

Here’s a simple checklist to help you get started right now:

-

Gather all financial data (income, expenses, savings, debts)

-

Identify personal risk factors (job loss, inflation, market dips)

-

Run “what if” scenarios in a spreadsheet or app

-

Evaluate how each scenario affects your finances

-

Strengthen weak points (increase savings, adjust investments, cut costs)

-

Repeat annually or after major life changes

Final Thoughts

Stress-testing your financial plan might not sound exciting, but it’s one of the smartest things you can do for your future. It turns uncertainty into clarity and fear into confidence.

Life is unpredictable but your financial stability doesn’t have to be. By proactively running through possible challenges, you’re not just planning for success you’re engineering it.

So go ahead, grab that spreadsheet, and start your financial stress test today. Your future self will thank you for it.

What's Your Reaction?

Like

0

Like

0

Dislike

0

Dislike

0

Love

0

Love

0

Funny

0

Funny

0

Angry

0

Angry

0

Sad

0

Sad

0

Wow

0

Wow

0