Vegan Options Propel Ready Meals Market Forward

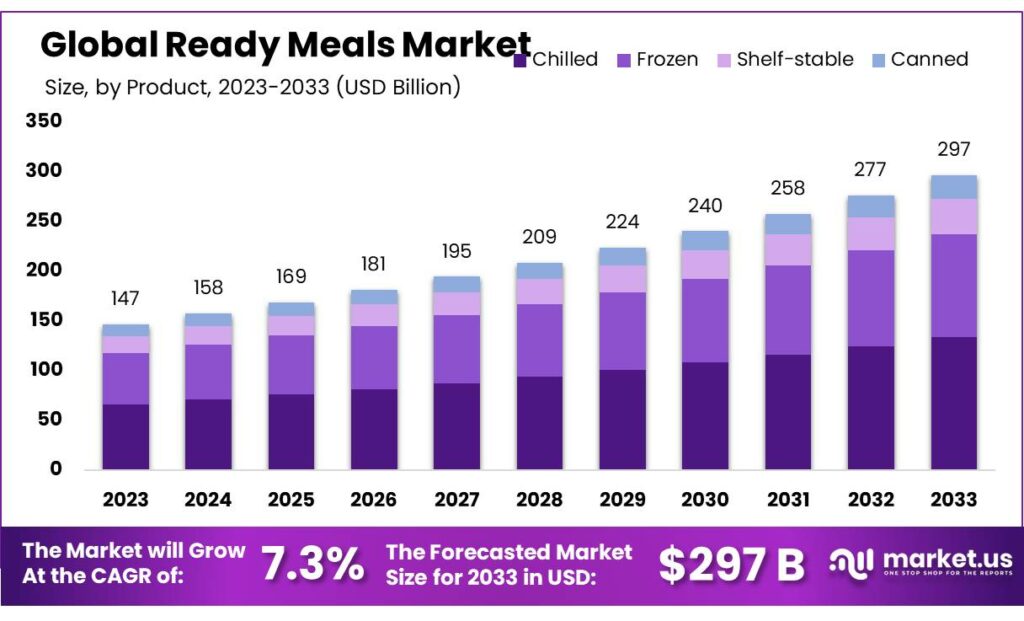

Global Ready Meals Market size is expected to be worth around USD 297 Billion by 2033 from USD 147 Billion in 2023, growing at a CAGR of 7.3%

Overview

Global Ready Meals Market size is expected to be worth around USD 297 Billion by 2033 from USD 147 Billion in 2023, growing at a CAGR of 7.3% during the forecast period from 2023 to 2032.

The ready meals market refers to the segment of the food industry focused on the production and sale of pre-packaged, pre-cooked meals that require minimal preparation before consumption. These meals cater to the growing demand for convenience among consumers who have busy lifestyles or limited time for cooking. The market includes a variety of options, such as frozen meals, refrigerated meals, and shelf-stable meals, encompassing a wide range of cuisines and dietary preferences.

Growth in the ready meals market is driven by several factors, including increasing urbanization, rising disposable incomes, and a shift in consumer preferences towards convenient and quick meal solutions. Additionally, technological advancements in food preservation and packaging have enhanced the quality and shelf-life of ready meals, further boosting their popularity. The market also benefits from the growing trend of single-person households and the need for easy-to-prepare meal options.

Despite its growth, the ready meals market faces challenges such as concerns over nutritional value, health implications of processed foods, and competition from fresh meal delivery services. However, companies in this market are continually innovating to address these concerns by offering healthier options, organic ingredients, and catering to specific dietary needs such as gluten-free, vegan, and low-calorie meals. The market's ability to adapt to changing consumer preferences and lifestyles will determine its future trajectory.

Key Market Segments

By Product

-

Chilled

-

Frozen

-

Shelf-stable

-

Canned

By Meal Type

-

Vegan

-

Vegetarian

-

Non-vegetarian

By Age Group

-

18-24 Years

-

25-34 Years

-

35-44 Years

-

45-54 Years

-

Above 55 Years

By End-use

-

Residential

-

Food Services

By Distribution Channel

-

Convenience Stores

-

Supermarkets & Hypermarkets

-

Online

-

Others

Download a sample report in MINUTES@https://market.us/report/ready-meals-market/

In 2023, chilled ready meals led the market with a 45.6% share, driven by their freshness and minimal processing, appealing to consumers seeking convenient and nutritious options with a shorter shelf life. Vegan ready meals held a 40.3% share, driven by growing interest in plant-based diets for health and environmental reasons, appealing to those seeking cruelty-free and sustainable food options.

The 18-24 years age group dominated the ready meals market, securing a 45.3% share, as young adults and college students prioritize convenience and quick meal solutions due to busy lifestyles and limited cooking skills. Food services emerged as the dominant segment, capturing a 65.4% share, including restaurants, cafeterias, catering services, and other food service providers catering to a wide range of consumers.

Supermarkets and hypermarkets dominated the retail segment of the ready meals market with a 46.7% share, offering a wide variety of ready meals and catering to diverse consumer preferences due to their convenient locations, extensive product range, and one-stop shopping experience.

Market Key Players

-

Nestlé

-

General Mills, Inc.

-

2 Sisters Food Group

-

Conagra Brands Inc.

-

Dr. Oetker

-

Green Mill Foods

-

Hormel Foods Corporation

-

Iceland Foods Ltd

-

McCain Foods Limited

-

Nomad Foods

-

The Campbell Soup

-

The JM Smucker Co.

-

The Kraft Heinz

-

Tyson Foods Inc

-

Tyson Foods, Inc.

-

Unilever

Driver: The primary driver for the ready meals market is the shift in consumer lifestyles towards more hectic and busy schedules, increasing the demand for convenient and time-saving meal options. Additionally, rising disposable incomes globally contribute to the growing popularity of ready meals, as consumers are more willing to spend on convenience.

Restraint: Fresh foods are considered superior alternatives to ready meals, and the rising popularity of fresh foods due to health consciousness and lifestyle disorder concerns serves as a significant restraint. The preference for fresh over packaged ready meals has been accelerated by recent developments during the COVID-19 pandemic.

Opportunity: The increasing popularity of ready meals, coupled with rising disposable incomes, presents lucrative growth opportunities for the market over the forecast period. Manufacturers can capitalize on this trend by introducing a variety of ready meal options that cater to diverse consumer preferences and dietary needs.

Challenge: The main challenge for the ready meals market is balancing convenience with health and nutritional value. As consumers become more health-conscious, ready meal producers must innovate to offer healthier options that compete with the perceived benefits of fresh foods. Ensuring high-quality, nutritious, and appealing ready meals is crucial to overcoming this challenge.